Triple A Whole Life Policy: A Comprehensive Guide To Secure Your Financial Future

Triple A Whole Life Policy has become an essential consideration for individuals seeking long-term financial security. As life expectancy continues to increase, securing a reliable insurance plan that offers lifelong coverage and guaranteed benefits has never been more crucial. This policy stands out as one of the most robust options available, combining insurance protection with wealth accumulation features. In this article, we will delve into the intricacies of Triple A Whole Life Policy, helping you understand its benefits, costs, and how it can fit into your financial strategy.

A whole life policy is more than just insurance; it's an investment in your future. The Triple A variant takes this concept further by offering advanced features that cater to modern financial needs. Whether you're planning for retirement, estate planning, or simply seeking peace of mind, this policy provides a solid foundation for your financial goals.

This guide aims to provide you with all the information you need to make an informed decision about Triple A Whole Life Policy. We'll explore its benefits, costs, and potential drawbacks, ensuring you have a clear understanding of what this policy entails.

Read also:Discovering Maureen Mccormick A Journey Through Her Life And Career

Table of Contents

- What is Triple A Whole Life Policy?

- Key Features of Triple A Whole Life Policy

- Benefits of Triple A Whole Life Policy

- Understanding the Costs

- Comparison with Other Policies

- Eligibility Criteria

- Investment Aspects

- Tax Implications

- The Claims Process

- Conclusion and Final Thoughts

What is Triple A Whole Life Policy?

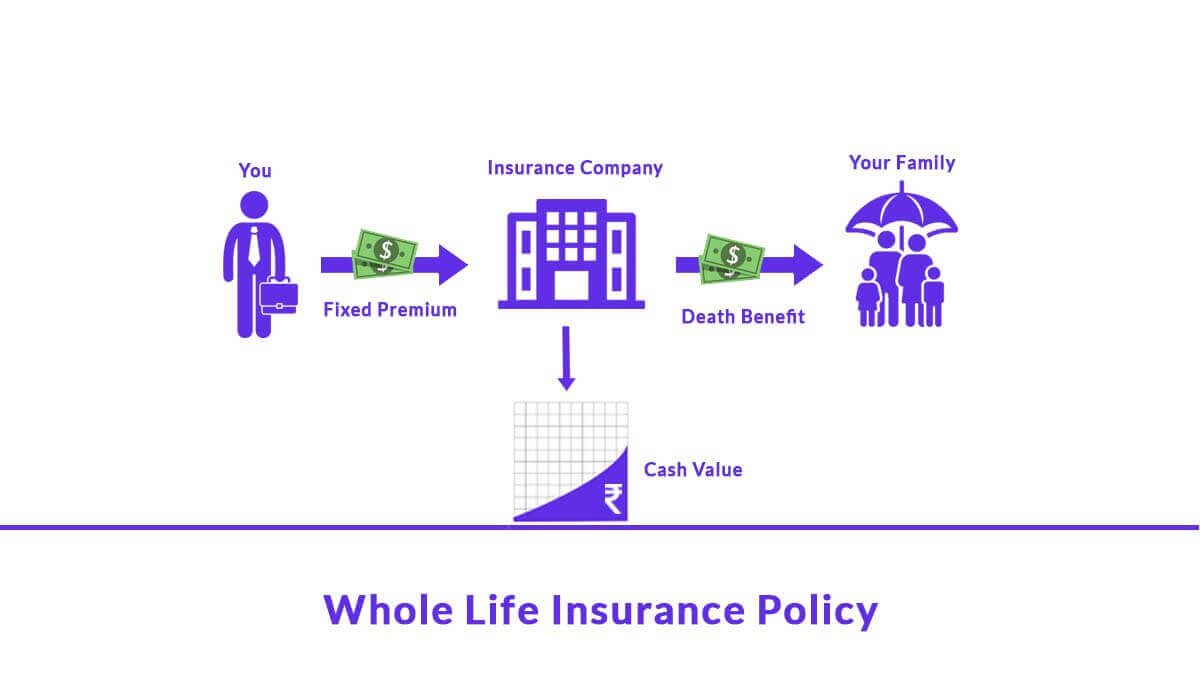

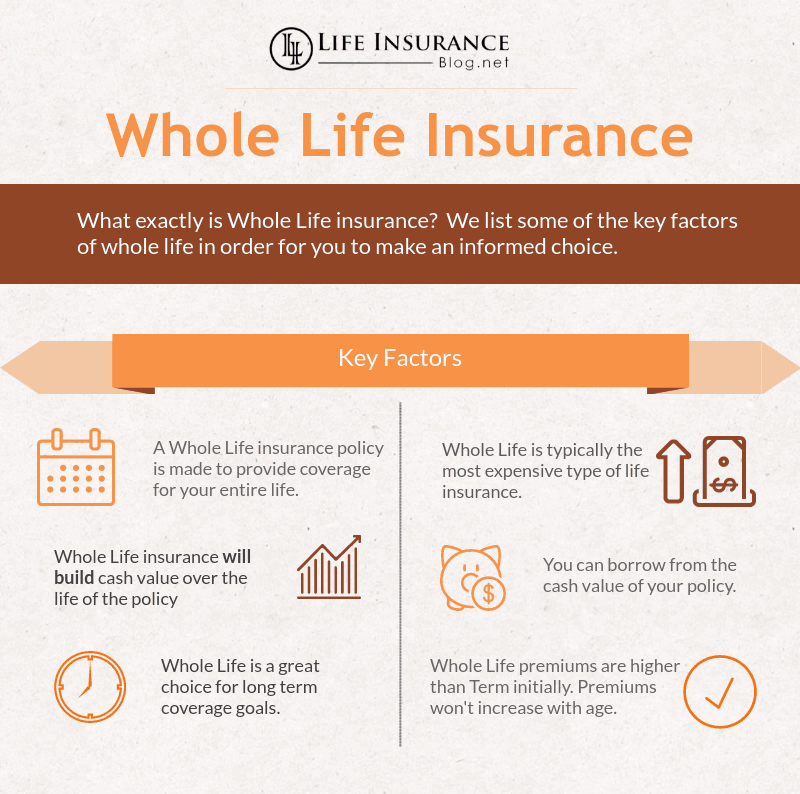

A Triple A Whole Life Policy is a type of permanent life insurance designed to provide lifelong coverage while also offering a savings component. Unlike term life insurance, which only provides coverage for a specific period, whole life policies remain active for the insured's entire lifetime, as long as premiums are paid.

Definition and Purpose

This policy is specifically crafted to address the financial needs of individuals seeking comprehensive coverage. It guarantees a death benefit to beneficiaries and builds cash value over time, making it an attractive option for those looking to combine insurance with investment.

How It Works

When you purchase a Triple A Whole Life Policy, you pay regular premiums that contribute to both the insurance coverage and the cash value of the policy. The cash value grows tax-deferred and can be accessed through loans or withdrawals, providing financial flexibility.

Key Features of Triple A Whole Life Policy

The Triple A Whole Life Policy comes with several standout features that make it a popular choice among insurance seekers. Below are some of the key aspects:

- Lifelong Coverage: The policy remains active for the insured's entire life.

- Guaranteed Death Benefit: Beneficiaries receive a predetermined payout upon the insured's passing.

- Cash Value Accumulation: A portion of the premiums contributes to the policy's cash value, which grows over time.

- Fixed Premiums: Premiums remain the same throughout the policy's duration, providing budgeting stability.

Benefits of Triple A Whole Life Policy

Choosing a Triple A Whole Life Policy offers numerous advantages that can significantly impact your financial well-being. Let's explore these benefits in detail:

Financial Security

One of the primary benefits is the assurance of financial security for your loved ones. The guaranteed death benefit ensures that your beneficiaries receive a payout, regardless of when you pass away.

Read also:Who Is Gretchen Hillmer Bonaduce Discover Her Inspiring Journey

Investment Growth

The policy's cash value component allows for investment growth, providing an additional financial cushion. This feature is particularly appealing for those looking to build wealth over time.

Tax Advantages

The cash value accumulates on a tax-deferred basis, meaning you don't pay taxes on the growth until you withdraw or borrow against it. This can be a significant advantage for long-term financial planning.

Understanding the Costs

While the benefits of a Triple A Whole Life Policy are substantial, it's important to understand the associated costs. Premiums for whole life policies are generally higher than those for term life insurance due to the additional features they offer.

Premium Structure

Premiums are calculated based on factors such as age, health, and the desired coverage amount. They remain fixed throughout the policy's duration, providing predictability in your financial planning.

Additional Fees

Some policies may include additional fees for riders or optional features. It's essential to review these costs carefully to ensure they align with your financial goals.

Comparison with Other Policies

When considering a Triple A Whole Life Policy, it's helpful to compare it with other types of insurance policies. Here's a brief overview:

Term Life Insurance

Term life insurance provides coverage for a specified period and typically costs less than whole life policies. However, it lacks the cash value component and may not offer lifelong coverage.

Universal Life Insurance

Universal life insurance offers more flexibility in terms of premium payments and coverage amounts. While it shares some similarities with whole life policies, it may not provide the same level of guarantees.

Eligibility Criteria

To qualify for a Triple A Whole Life Policy, you must meet certain eligibility criteria. These typically include age requirements, health assessments, and income verification. Insurers evaluate these factors to determine your premium rates and coverage options.

Investment Aspects

The investment component of a Triple A Whole Life Policy is one of its most attractive features. Here's how it works:

How Cash Value Grows

Cash value grows through interest credited to the policy. The rate of growth depends on the insurer's investment performance and the policy's terms.

Accessing Cash Value

You can access the cash value through policy loans or withdrawals. It's important to note that accessing the cash value may impact the death benefit and could result in taxable income.

Tax Implications

Understanding the tax implications of a Triple A Whole Life Policy is crucial for effective financial planning. Here are some key points:

Tax-Deferred Growth

The cash value grows tax-deferred, meaning you don't pay taxes on the growth until you withdraw or borrow against it.

Tax on Withdrawals

Withdrawals from the policy may be subject to taxation if they exceed the amount of premiums paid. It's advisable to consult with a tax professional to understand the specific implications for your situation.

The Claims Process

When the time comes to file a claim, understanding the process is essential. Here's a brief overview:

Steps to File a Claim

1. Notify the insurance company of the insured's passing.

2. Submit the required documentation, including a death certificate.

3. The insurer will review the claim and issue the payout to the beneficiaries.

Common Issues

Issues such as policy lapses or disputes over coverage can arise. It's important to maintain accurate records and communicate with your insurer to resolve any concerns promptly.

Conclusion and Final Thoughts

In conclusion, a Triple A Whole Life Policy offers a comprehensive solution for individuals seeking lifelong coverage and investment growth. Its guaranteed death benefit, cash value accumulation, and tax advantages make it a valuable addition to any financial portfolio.

We encourage you to take action by exploring this policy further and consulting with a financial advisor to determine if it aligns with your goals. Share your thoughts and experiences in the comments below, and don't hesitate to explore other articles on our site for more insights into financial planning.

For more information, refer to trusted sources such as the Securities and Exchange Commission and the Internal Revenue Service for detailed guidance on insurance policies and tax implications.

{kind=link}